August 2024 Review

Destra Capital

September 3, 2024August Year-To-Date Macro Markets

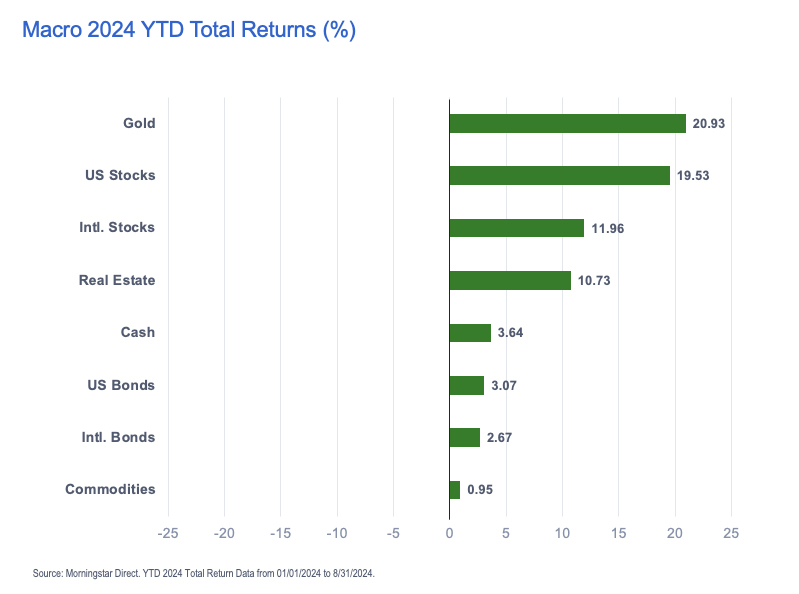

Stocks

In the old classic 60/40 model, stocks make up the majority of the allocation. Through the end of August, that part of the balanced model has performed brilliantly, up an astounding almost 20% YTD (S&P 500 19.53%).

But the risks embedded in that allocation are growing dramatically.

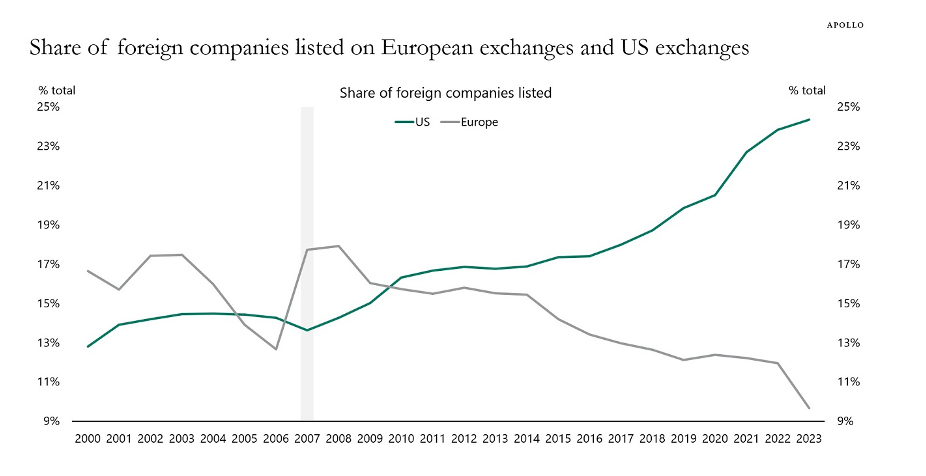

Give Us Your Tired, Your Hungry, Your Free-Float Adjusted… Consider that more and more of the worlds stocks are moving to the US, as shown here in a graphic from Apollo where US listings reflect the NYSE and NASDAQ US and European listing include LSE, Euronext, Deutsche Boerse AG and NASDAQ Nordic.

Source: World Federation of Exchanges, Apollo Chief Executive

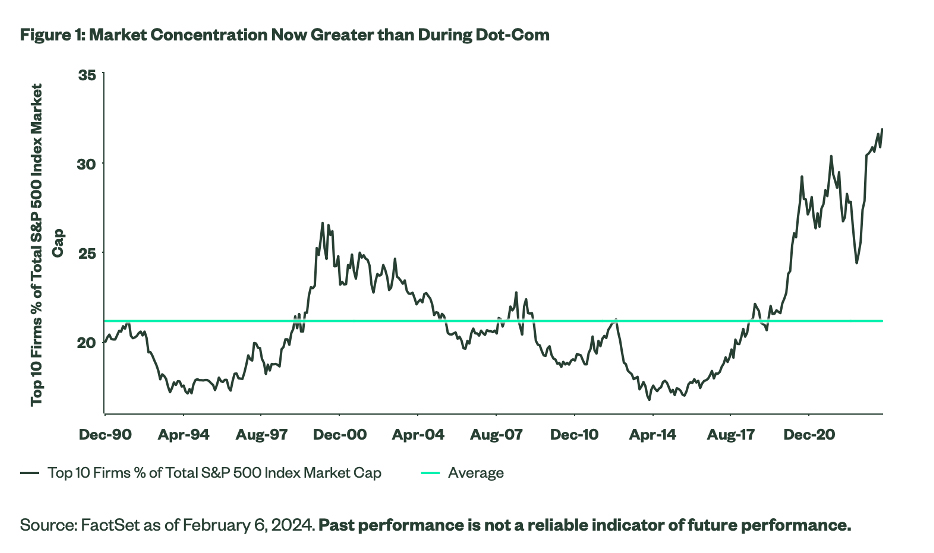

From Concentrate. And the stocks within the US are getting more and more concentrated in just a few ultracap tech and AI names…

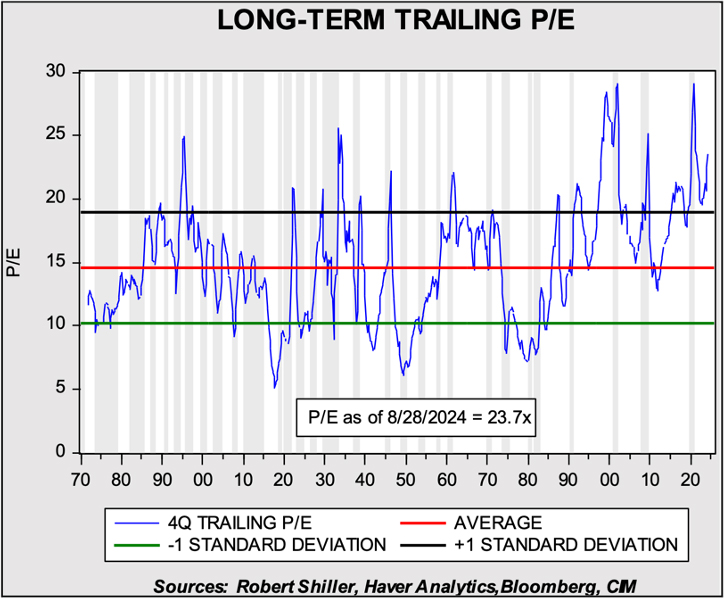

High As a Kite. Which is pushing valuations on the whole asset class into the stratosphere…..

And since study after study reminds us that future returns are highly correlated to starting valuations, one has to think that a healthy dose of stocks in a portfolio right now should be offset by…..

Bonds

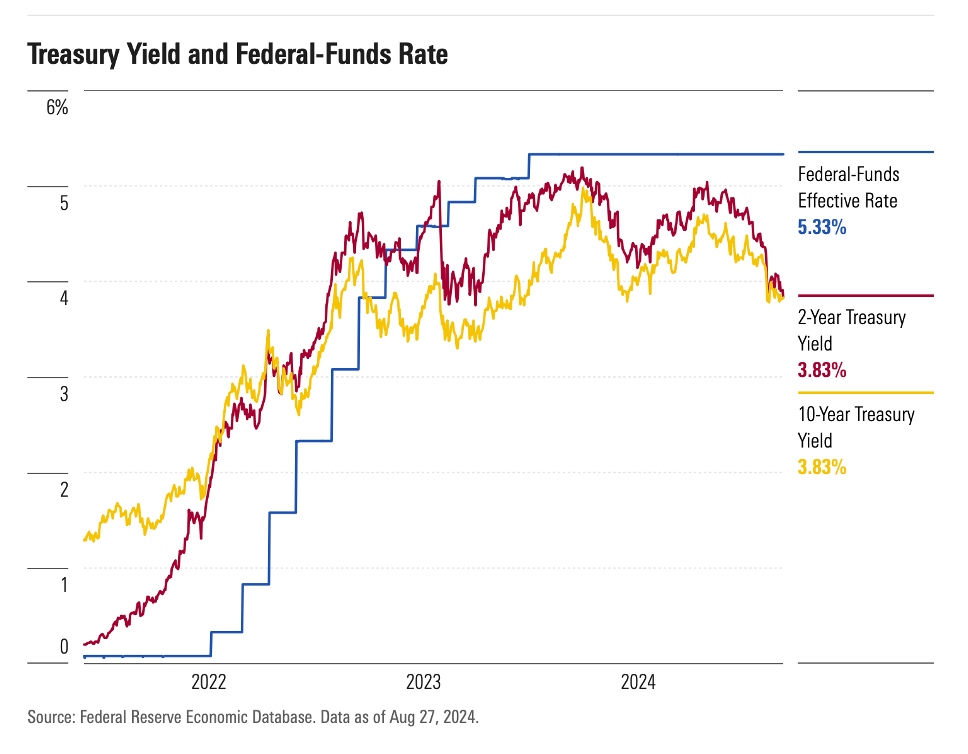

The 3.83% to Yuma. The Fed has all but promised that rates will fall with the leaves beginning in mid September. Whether the cut is 25 bps, 50 bps or more is open to a lot of debate and posturing all along the rate curve right now. As the graphic below from Morningstar shows, the market for 2’s and 10’s are anticipating a significant move down by The Fed.

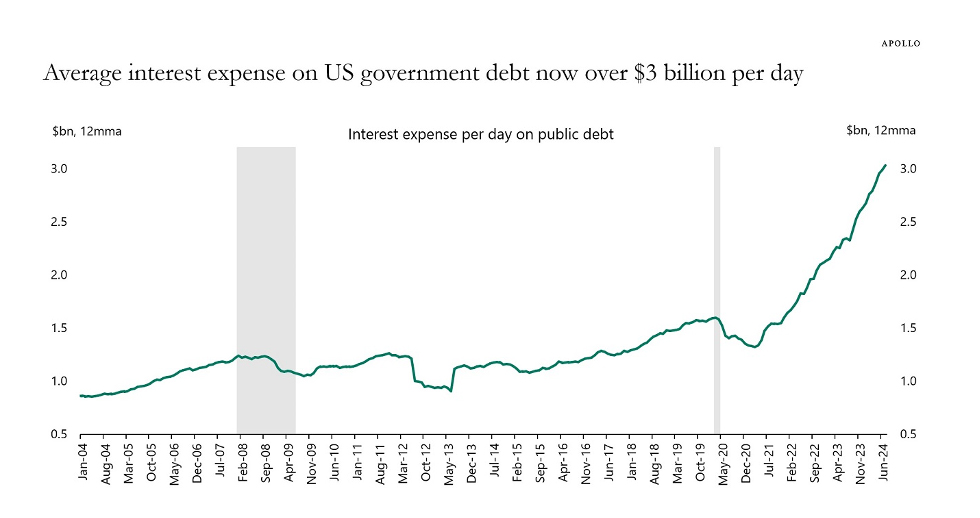

My Debt Is Just So Much More Outstanding Than Yours. Relief from higher rates can’t come soon enough to the US government debt market where we Americans pay a whopping $3 billion every day for the privilege of having so much outstanding debt. For the curious, this data from Haver Analytics and Apollo includes weekends! No rest for the debt weary. (Of course this is sustainable…..why would you even ask that, comrade?)

Source: US Treasury, Haver Analytics, Apollo Chief Economist

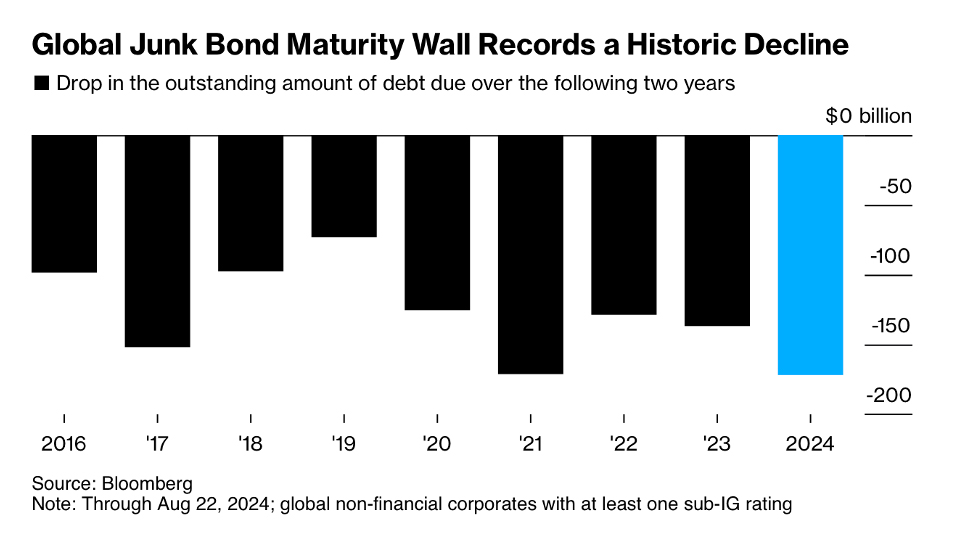

A Few Bricks Short Of A Full Load. According to Bloomberg, “The feared maturity wall (in high yield) is proving more of a speed bump, with the world’s junk bond market so far this year seeing the biggest decline in looming debt repayments in at least a decade.”

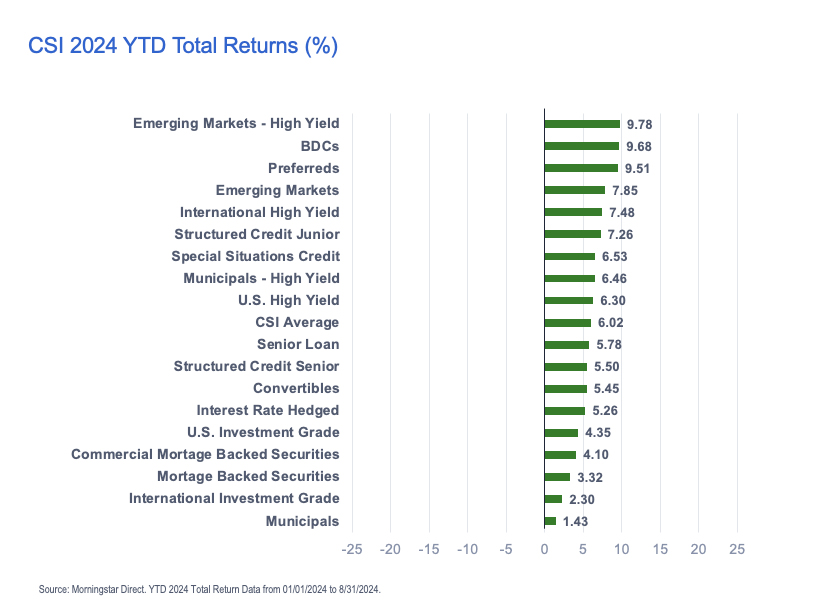

And this enthusiasm for leveraged finance in all its permutations is borne out in the year-to-date returns for different credit investing strategies as shown in the August Destra Credit Strategies Indicator below.

Year-to-Date Credit Strategies Indicator

While US High Yield and Senior Loan strategies have returned an attractive 6.30% and 5.78% respectively year to date, alternative credit strategies that structure or refinance or originate leveraged finance have done even better through August 31st. BDC strategies were up a staggering 9.68%, Structured Credit Junior Tranches delivered 7.26% and Special Situations Credit has returned 6.53%.

With summer coming to an end, so too should the wait for lower short term US rates. It will be very interesting to see if equity and high yield markets are encouraged by a rate cut and continue to move prices higher, or if the underlying risk of a slowing economy makes its way into the price expectations for risk assets this September.

We will be back in early October to recap how this month plays out for the Destra CSI and markets in general.